If you’ve spent any time reading about investing or watching financial news, you’ve heard this phrase over and over:

“The S&P 500 is up today.” “The market dropped 2% — the S&P 500 fell sharply.” “Just invest in the S&P 500 and forget about it.”

But what actually is the S&P 500? Why does everyone treat it like the be-all and end-all of investing? And how do you actually invest in it?

Let’s break it down.

What is the S&P 500?

The S&P 500 is a stock market index — a list of 500 of the largest publicly traded companies in the United States, weighted by their market value.

“S&P” stands for Standard & Poor’s, the financial company that created and maintains the index. The “500” refers to the approximately 500 companies included.

Think of the S&P 500 as a report card for the U.S. economy. When the S&P 500 goes up, it means the largest American companies are collectively doing well. When it goes down, it signals that the market — and often the broader economy — is struggling.

How Did the S&P 500 Start?

The S&P 500 was officially launched on March 4, 1957, by Standard & Poor’s. However, its roots go back to 1923, when S&P first began tracking a small group of U.S. stocks.

Before the S&P 500 existed, investors mostly followed the Dow Jones Industrial Average (DJIA) — an index of just 30 large companies, created in 1896. But 30 companies wasn’t nearly enough to represent the entire U.S. stock market.

The S&P 500 was designed to give a much broader, more accurate picture of market performance — and it quickly became the standard benchmark that investors, economists, and financial professionals use to measure the health of the U.S. stock market.

Which Companies Are in the S&P 500?

To be included in the S&P 500, a company must meet several criteria:

- Be a U.S.-based public company

- Have a market capitalization of at least $18 billion

- Be profitable over the most recent quarter and the trailing 12 months

- Have its shares readily available for public trading

As of 2025, some of the largest companies in the S&P 500 include:

| Company | Ticker | Sector |

|---|---|---|

| Apple | AAPL | Technology |

| Microsoft | MSFT | Technology |

| NVIDIA | NVDA | Technology |

| Amazon | AMZN | Consumer/Tech |

| Alphabet (Google) | GOOGL | Technology |

| Meta (Facebook) | META | Technology |

| Berkshire Hathaway | BRK.B | Financials |

| JPMorgan Chase | JPM | Financials |

| Eli Lilly | LLY | Healthcare |

| Visa | V | Financials |

The index is market-cap weighted, meaning larger companies have a bigger influence on the index’s movement. Apple and Microsoft alone account for roughly 7% of the entire index — so when these giants move, the whole index feels it.

How is the S&P 500 Different from the Stock Market?

This is a common source of confusion. People say “the market is up” when they mean “the S&P 500 is up” — but they’re not exactly the same thing.

The U.S. stock market contains over 5,000 publicly traded companies. The S&P 500 only includes 500 of them — but these 500 companies represent approximately 80% of the total value of the entire U.S. stock market.

So while the S&P 500 isn’t literally the whole market, it’s close enough that most investors treat it as a reliable proxy. When people say “the market,” they almost always mean the S&P 500.

Why Does Everyone Talk About the S&P 500?

Because over the long term, it has delivered remarkable results.

Here’s what the S&P 500 has done historically:

| Time Period | Average Annual Return |

|---|---|

| Since 1957 (inception) | ~10.5% per year |

| Last 30 years | ~10.7% per year |

| Last 10 years | ~13.1% per year |

To put that in perspective:

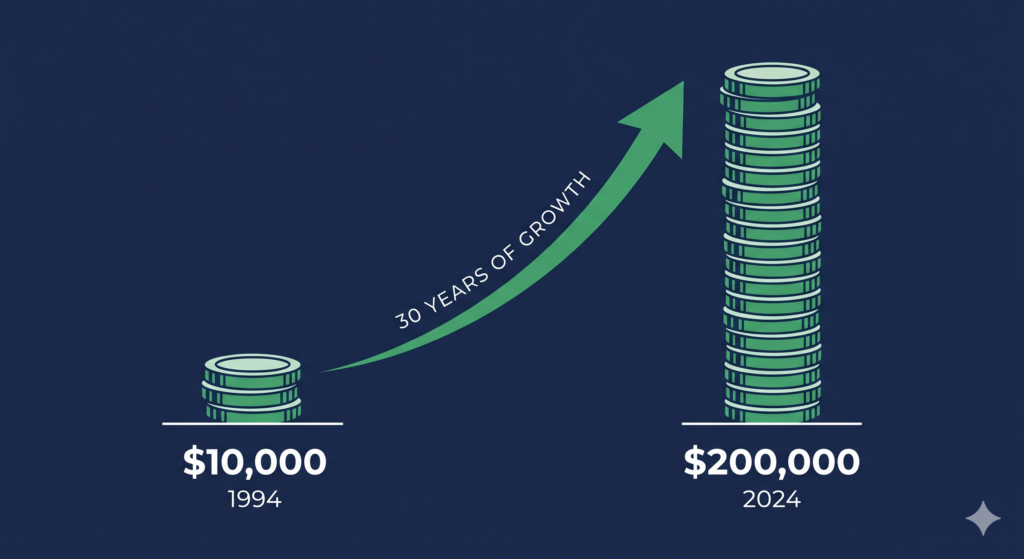

If you had invested $10,000 in an S&P 500 index fund in 1994 and never touched it, by 2024 it would have grown to approximately $200,000 — purely through market growth and reinvested dividends.

That’s not a typo. $10,000 → $200,000 in 30 years, without picking a single stock.

This is why Warren Buffett — widely considered the greatest investor of all time — has repeatedly said that for most people, a low-cost S&P 500 index fund is the best investment they can make.

What Happens When the S&P 500 Drops?

Drops happen — and they’re a normal part of investing. Here’s some historical context:

| Event | S&P 500 Drop | Recovery Time |

|---|---|---|

| 2000–2002 Dot-com Crash | -49% | ~7 years |

| 2008–2009 Financial Crisis | -57% | ~5.5 years |

| 2020 COVID Crash | -34% | ~5 months |

| 2022 Rate Hike Selloff | -25% | ~1 year |

Notice something? The S&P 500 has recovered from every single crash in its history.

The investors who lost money permanently were those who panic-sold during the drops. The investors who stayed patient — or even bought more during the dips — came out ahead every time.

This is the core argument for long-term index investing: you don’t need to predict the market. You just need to not panic.

How Do You Actually Invest in the S&P 500?

You can’t directly buy “the S&P 500” — it’s just an index, a list. But you can buy ETFs and index funds that track it.

The most popular S&P 500 ETFs are:

VOO — Vanguard S&P 500 ETF

- Expense ratio: 0.03%

- One of the most popular ETFs in the world

- Ideal for long-term investors

SPY — SPDR S&P 500 ETF Trust

- Expense ratio: 0.0945%

- The oldest ETF in the U.S. (launched 1993)

- Most heavily traded ETF in the world

IVV — iShares Core S&P 500 ETF

- Expense ratio: 0.03%

- BlackRock’s version; nearly identical to VOO

All three track the same index — the S&P 500. The main differences are the expense ratio (annual fee) and the company that manages them. For long-term buy-and-hold investors, VOO and IVV are typically preferred due to their rock-bottom fees.

We’ll do a full deep-dive comparison of VOO vs SPY vs IVV in a future post.

S&P 500 vs. Other Indexes

The S&P 500 isn’t the only index out there. Here’s how it compares to other popular ones:

| Index | Companies | Focus |

|---|---|---|

| S&P 500 | 500 | Large U.S. companies |

| Dow Jones (DJIA) | 30 | 30 selected blue-chip companies |

| NASDAQ-100 | 100 | Top 100 NASDAQ companies (mostly tech) |

| Russell 2000 | 2,000 | Small U.S. companies |

| Total Stock Market | ~3,500+ | Nearly all U.S. public companies |

The S&P 500 sits in the sweet spot — broad enough to be representative, focused enough on established companies to be relatively stable.

Is the S&P 500 Right for Every Investor?

For most long-term investors, yes — it’s an excellent foundation. But it’s worth knowing a few limitations:

It’s U.S.-only. The S&P 500 only covers American companies. International diversification requires additional investments.

It’s large-cap heavy. Small and mid-sized companies are not well represented. Some investors prefer broader total market funds like VTI for this reason.

It’s tech-heavy. The top 10 holdings are heavily concentrated in technology. A major tech downturn would hit the index hard.

It doesn’t guarantee short-term gains. Over any given 1–3 year period, the S&P 500 can and does lose money. It’s a long-term vehicle.

Despite these limitations, for most everyday investors building long-term wealth, the S&P 500 remains one of the most reliable tools available.

Key Terms to Remember

| Term | Simple Definition |

|---|---|

| S&P 500 | An index tracking 500 of the largest U.S. companies |

| Index | A list of stocks used to measure market performance |

| Market cap | Total value of a company’s shares (price × shares outstanding) |

| Market-cap weighted | Larger companies have more influence on the index |

| Benchmark | A standard used to measure investment performance |

| VOO / SPY / IVV | Popular ETFs that track the S&P 500 |

Final Thoughts

The S&P 500 isn’t just a number on a screen. It’s a reflection of the U.S. economy, a benchmark for professional investors, and for many everyday people — the foundation of their entire investment strategy.

Understanding what it is and how it works is one of the most important things you can learn as a new investor.

In the next post, we’ll go one level deeper and look at the most popular S&P 500 ETF in the world: VOO. What is it exactly, how does it work, and is it the right choice for you?

See you there.

— BaselineJay

Disclaimer: This post is for informational and educational purposes only. While the author is a licensed CPA, this content does not constitute professional financial, investment, or tax advice. Always consult a qualified professional for advice specific to your situation.

Previously: What is an ETF? How It Works and Why It Matters ←