You’ve learned what ETFs are. You know VOO. You’ve seen how VOO and QQQ compare.

Now there’s another fork in the road that every investor eventually faces:

Do I want Growth ETFs or Dividend ETFs?

It sounds like a technical question, but it’s really a personal one. The answer depends on where you are in life, what you need your money to do, and how you think about building wealth.

Let’s break it down clearly.

The Core Difference

At the most basic level:

- Growth ETFs focus on companies that are reinvesting their profits to grow faster. They rarely pay dividends. You make money when the stock price goes up.

- Dividend ETFs focus on companies that share their profits with investors through regular cash payments (dividends). You make money through both price appreciation AND regular income.

Think of it this way:

Growth ETF = You plant a tree and wait for it to grow tall. Your wealth builds in the tree itself.

Dividend ETF = You plant a fruit tree. It grows, but also gives you fruit every few months. Your wealth builds in the tree AND you get fruit along the way.

Neither is better in absolute terms — they serve different purposes.

What is a Growth ETF?

A growth ETF holds companies that are expected to grow their revenues and earnings faster than the overall market.

These companies typically:

- Reinvest all profits back into the business

- Pay little to no dividends

- Have higher valuations (investors pay a premium for future growth)

- Are often in technology, healthcare, and consumer discretionary sectors

Popular Growth ETFs:

| ETF | What it tracks | Expense Ratio |

|---|---|---|

| VUG (Vanguard Growth ETF) | U.S. large-cap growth stocks | 0.04% |

| QQQ (Invesco QQQ Trust) | Nasdaq-100 (tech-heavy) | 0.20% |

| SCHG (Schwab U.S. Large-Cap Growth ETF) | U.S. large-cap growth | 0.04% |

| IWF (iShares Russell 1000 Growth ETF) | Russell 1000 growth stocks | 0.19% |

You’ll notice QQQ from our last post here — it’s essentially a growth ETF with a tech focus.

Top holdings in a typical growth ETF: Apple, Microsoft, NVIDIA, Amazon, Meta, Tesla — companies that reinvest heavily and grow fast.

What is a Dividend ETF?

A dividend ETF holds companies that pay regular dividends — quarterly cash payments to shareholders as a share of the company’s profits.

These companies typically:

- Are well-established, mature businesses

- Generate consistent, predictable cash flows

- Have a track record of paying (and often growing) dividends

- Are often in sectors like utilities, financials, consumer staples, and real estate

Popular Dividend ETFs:

| ETF | What it tracks | Dividend Yield | Expense Ratio |

|---|---|---|---|

| VYM (Vanguard High Dividend Yield ETF) | High dividend U.S. stocks | ~2.8% | 0.06% |

| SCHD (Schwab U.S. Dividend Equity ETF) | Quality dividend stocks | ~3.5% | 0.06% |

| DVY (iShares Select Dividend ETF) | High dividend U.S. stocks | ~4.5% | 0.38% |

| VIG (Vanguard Dividend Appreciation ETF) | Dividend growth stocks | ~1.8% | 0.06% |

Top holdings in a typical dividend ETF: Johnson & Johnson, JPMorgan Chase, Procter & Gamble, Coca-Cola, ExxonMobil — household names with decades of dividend history.

Performance Comparison: Growth vs Dividend

Over the past decade, growth ETFs have significantly outperformed dividend ETFs — largely driven by the technology boom.

| Period | VUG (Growth) | SCHD (Dividend) |

|---|---|---|

| 1 year (2024) | +33% | +13% |

| 3 years (2022–2024) | +30% total | +12% total |

| 5 years (2020–2024) | +115% total | +70% total |

| 10 years (2015–2024) | +310% total | +175% total |

Growth ETFs win on total return — but this comparison misses something important.

Dividend ETFs also pay you cash along the way. That $70 cash dividend per $2,000 invested in SCHD every year? It compounds when reinvested, and it also provides real income without selling shares.

Also: during market downturns, dividend ETFs tend to fall less than growth ETFs.

| Downturn | VUG Drop | SCHD Drop |

|---|---|---|

| 2022 Rate Hike Selloff | -33% | -6% |

| 2020 COVID Crash | -31% | -28% |

In 2022, growth investors watched their portfolios drop by a third while dividend investors barely felt it. Stability has real value — especially for investors who can’t stomach big swings.

The Tax Angle — A CPA’s Perspective

Since taxes are my day job, I want to flag something important that most investing blogs gloss over.

Dividends are taxable in the year you receive them — even if you reinvest them immediately.

- Qualified dividends (most dividends from U.S. stocks held long enough) are taxed at the lower long-term capital gains rate: 0%, 15%, or 20% depending on your income.

- Ordinary dividends are taxed at your regular income tax rate — potentially as high as 37%.

Growth ETFs, on the other hand, don’t pay much in dividends. You’re taxed only when you sell — and only on the gain. This means you control when you pay taxes, which is a significant advantage for high-income earners.

Bottom line from a tax perspective:

- In a taxable brokerage account: Growth ETFs are generally more tax-efficient

- In a tax-advantaged account (IRA, 401k): Dividend ETFs shine here because dividends aren’t taxed immediately — the cash compounds freely

This is something most investment content doesn’t mention clearly enough. Always consider your tax situation.

Who Should Choose Growth ETFs?

Growth ETFs are a better fit if you:

- ✅ Are in your 20s, 30s, or 40s — long time horizon ahead

- ✅ Don’t need income from your investments right now

- ✅ Are comfortable with higher volatility

- ✅ Are in a high tax bracket (growth is more tax-efficient in taxable accounts)

- ✅ Believe technology and innovation will continue driving returns

- ✅ Are focused on maximizing total wealth at a future date

Who Should Choose Dividend ETFs?

Dividend ETFs are a better fit if you:

- ✅ Are in or approaching retirement — want regular income

- ✅ Want cash flow without selling shares

- ✅ Prefer lower volatility and steadier performance

- ✅ Are holding in a tax-advantaged account (IRA, 401k)

- ✅ Want to reinvest dividends to compound over time

- ✅ Like the psychological comfort of getting paid regularly

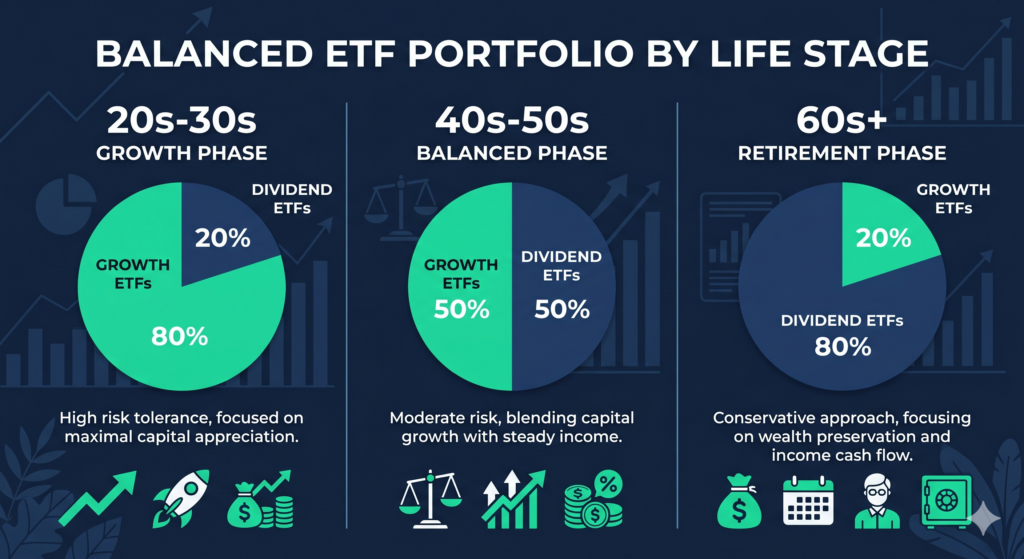

The Smart Approach: Use Both

Most savvy investors don’t choose one or the other — they use both, in proportions that match their life stage.

A common framework:

Early career (20s–30s):

70–80% Growth ETFs (VUG, QQQ)

20–30% Broad market (VOO, VTI)

Minimal dividend focus

Mid-career (40s–50s):

50–60% Growth/Broad market (VOO, VUG)

20–30% Dividend ETFs (SCHD, VYM)

10–20% Bonds for stability

Retirement (60s+):

30–40% Broad market (VOO)

40–50% Dividend ETFs (SCHD, VYM, DVY)

20–30% Bonds

This isn’t a one-size-fits-all prescription — but it illustrates how the balance shifts as income needs change.

SCHD: The Dividend ETF Worth Knowing

If you only remember one dividend ETF from this post, make it SCHD — the Schwab U.S. Dividend Equity ETF.

SCHD is beloved in the dividend investing community for good reason:

- Low cost: 0.06% expense ratio

- Quality focused: screens for dividend growth, financial strength, and yield consistency — not just the highest yielders

- Dividend growth: SCHD has consistently grown its dividend payout year over year

- Historical performance: One of the best risk-adjusted returns of any dividend ETF

SCHD isn’t just a high-yield fund — it’s a quality fund that happens to pay a growing dividend. That distinction matters enormously over the long term.

Key Terms to Remember

| Term | Simple Definition |

|---|---|

| Growth ETF | ETF focused on fast-growing companies that reinvest profits |

| Dividend ETF | ETF focused on companies that pay regular cash dividends |

| Dividend yield | Annual dividend as a % of share price |

| Qualified dividend | Dividend taxed at lower capital gains rate |

| SCHD | Popular dividend ETF known for quality and dividend growth |

| VUG | Popular growth ETF from Vanguard |

| Tax-advantaged account | IRA or 401k — dividends grow tax-free or tax-deferred |

Final Thoughts

Growth vs. Dividend isn’t a competition — it’s a spectrum. Where you sit on that spectrum should reflect your age, income needs, tax situation, and risk tolerance.

If you’re young and building wealth: lean growth. If you’re approaching retirement and need income: lean dividend. If you’re somewhere in the middle: blend both.

The most important thing is to be intentional about your choice — and to understand what you own and why.

In the next post, we’re heading back to baseball — where we’ll dive into the advanced batting statistics that sabermetrics introduced: wOBA, wRC+, OPS+, and more. These are the numbers that modern front offices actually use to evaluate hitters.

See you there.

— BaselineJay, CPA

This post is for informational and educational purposes only. While the author is a licensed CPA, this content does not constitute professional financial, investment, or tax advice. Always consult a qualified professional for advice specific to your situation.

Previously: VOO vs QQQ: Which ETF Should You Buy? ←

Up Next: [Advanced Batting Stats Explained: wOBA, wRC+, OPS+ and More →]